December Update

Happy New Year to everyone. I hope you enjoyed the holidays with your loved ones.

This is my late update for December. Going into 2026, I want to go back to what I enjoy the most: micro caps.

2025 was a great year for me overall, although I gave some of it back in November (I mentioned this in my update that month). I tried short term options, Biotech, a lot of leverage, etc. and It was fun, but it also came with anxiety — lots of volatility, big moves up and down, and emotional swings.

I think 2026 could look similar: we may see big drawdowns like April and November, but also strong rallies. Instead of trying to chase the next “hot trade,” I want to focus on what I like best: small companies with real profits, low debt, good management, and niche markets.

You’ll still see a couple of positions that don’t fully match that checklist (like Ethereum and Evolv). For me, those are more like trades, and I expect to close them in the short term unless the story improves a lot.

Long term, I want to own companies where it’s hard to build a position (illiquid) and also hard to exit. That forces me to be more selective and patient.

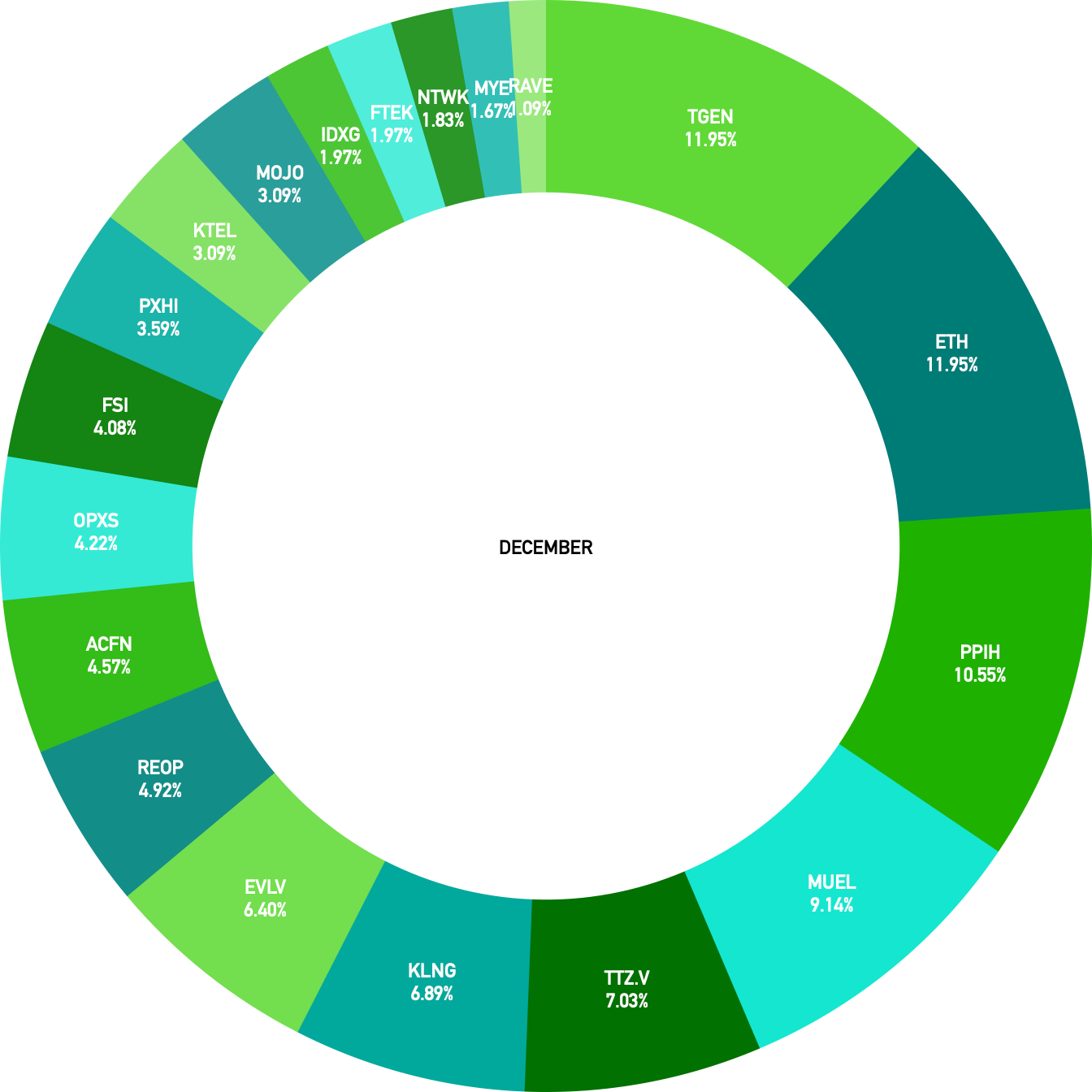

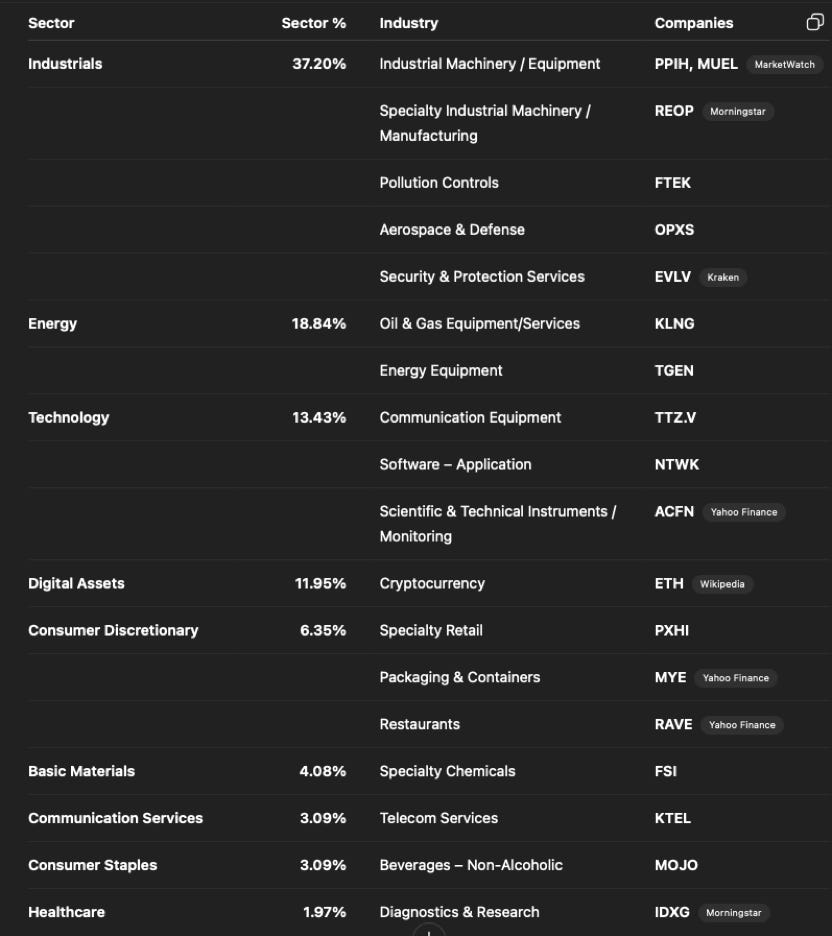

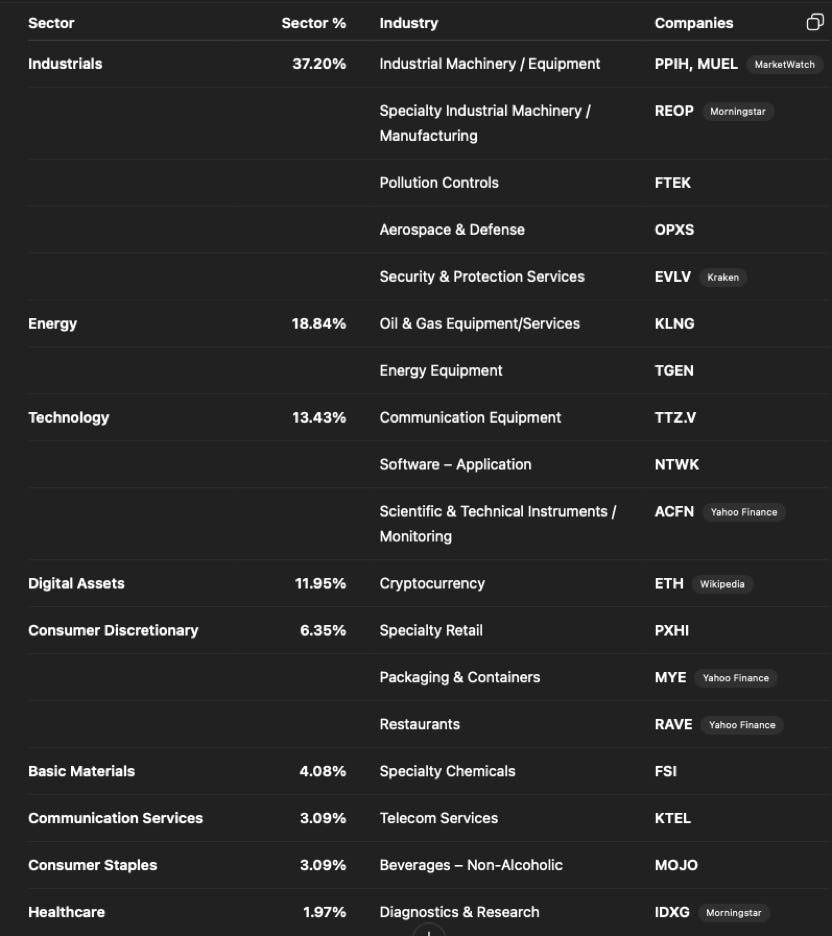

As of January 6, 2026, the portfolio is around 20 positions, which is a number I feel comfortable owning. Some weights will likely change over time (for example, I feel a bit overweight in TGEN), but overall I like how it looks.

Not financial advice. This is mainly for my own accountability. But knowing someone is reading also pushes me to keep writing. Please do your own research.

TGEN — 11.95%

ETH — 11.95%

PPIH — 10.55%

MUEL — 9.14%

TTZ.V — 7.03%

KLNG — 6.89%

EVLV — 6.40%

REOP — 4.92%

ACFN — 4.57%

OPXS — 4.22%

FSI — 4.08%

PXHI — 3.59%

KTEL — 3.09%

MOJO — 3.09%

IDXG — 1.97%

FTEK — 1.97%

NTWK — 1.83%

MYE — 1.67%

RAVE — 1.09%

Portfolio Changes

Buys

Bought: MYE, REOP, RAVE, IDXG

Re-entered: ACFN

Sells

Sold: VELO

Sell Notes

VELO

I really like the company and what they are building, and I plan to re-enter in the future. But the valuation moved too fast. I’ve seen this kind of move before (for example with TGEN), and usually there are opportunities again later.

I started buying around $5 and sold around $11.50, which was a great run in about 1.5 months.

Currently the stock is trading near $20, which I think is a crazy rally. They also lowered their 2025 revenue to around $45–$55M (if I remember correctly), so at these prices the stock is trading at almost ~8× sales. The future still looks bright, and 50% YoY growth may be possible, but for me it’s too much. I prefer to buy this kind of company at more reasonable valuations, so I took the win and I’ll watch for a better re-entry later.

Holdings — News & Notes

TGEN — Tecogen

TGEN has been a roller coaster lately. I think there’s a lot of noise in the market, and this is a very binary position — basically zero or hero.

I like the technology, but as a shareholder I want to see real purchase orders. That’s what will confirm where the business is going. Until then, it’s still more of a great story than a proven business, even if the “picks and shovels” angle and the data center theme are very strong right now.

I added shares recently, which is why it became my #1 position. The stock dropped around 20% at one point, then IR posted comments on LinkedIn that helped explain the situation. People I respect on X were also defending the thesis, so I don’t feel alone here.

That said, I’m not blindly holding. I have a clear rule: if the thesis changes, or if there’s no meaningful progress by the end of the year, I’ll cut it — whether I’m up or down.

PPIH — Perma-Pipe International

Perma-Pipe ($PPIH) delivered a very strong quarter. Revenue came in at $61.1M, up ~47% YoY, clearly ahead of expectations. They booked $52M in new awards, and despite the strong revenue, backlog still grew to $148.9M, higher than earlier this year and well above last year’s levels. Growth was driven by continued strength in North America and the Middle East, with large projects tied to Saudi Aramco and Qatar. CEO David Mansfield summed it up well: “We are experiencing strong demand across multiple markets and regions, driven by increased activity in North America and the Middle East.”

Margins also stood out, with gross margin rebounding to 34%, showing real operating leverage as volumes scale. That said, I don’t think we can automatically take this $0.77 EPS as a clean run rate yet — it’s still too early to say how sustainable it is. What matters most from here is backlog conversion and whether margins hold. For context, in Q4 2024the company did around $45M in revenue and $0.22 in EPS, so they shouldn’t have any issue beating those numbers next quarter. If they manage to do ~$3 in EPS in 2026, which I think is possible, the stock is trading at roughly a 10x forward P/E at current prices. Looking ahead, a 15–20x multiple feels fair for a company with a solid balance sheet, strong backlog, and improving execution — but we’ll know a lot more once we see how the next quarter plays out.

MUEL — Paul Mueller Company

No recent news. The stock has been drifting lower, but that’s normal for MUEL.

It’s extremely illiquid (~900k shares outstanding, and often ~100 shares/day in volume). Small trades can move the price a lot.

Technically it’s near the 200-day moving average, so I’m watching that level. Valuation looks attractive: around $50 EPS, so roughly ~8× earnings at current prices.

TTZ.V — Total Telcom

No recent news.

Here’s a nice thread if you want to read a bit more on the company

Juan Pablo Montero@jpmontero88

Let’s talk about $TTZ.V $TTLTF

The investment opportunity here can be best understood through the lens of the company’s current inflection point, which management itself highlights clearly:

“a business that is now consistently profitable, cash-generative, and positioned to

Juan Pablo Montero @jpmontero88

$TTZ.V $TTLTF 👀 https://t.co/IK3NAk2McC

11:39 AM · Dec 19, 2025 · 4.24K Views

1 Reply · 2 Reposts · 9 Likes

KLNG — KOIL Energy Solutions

KLNG delivered a mixed but constructive Q3, posting $6.4M in revenue, up 22% YoY, with both services and product sales contributing to the growth. CEO Eric Wieck opened the call by emphasizing that “Coil Energy is growing again,” pointing to strong order intake and expanding traction in renewables, including a wind-farm cable-spooling project that earned “excellent feedback during the ongoing project execution.” The company also announced its first two contracts in Brazil, small in size but strategically important as they establish a local foothold in a deepwater market with long-term potential.

The downside of the quarter was the hit to profitability. Gross profit held steady at $2.1M, but margins compressed to 32% due to a heavier mix of pass-through costs. SG&A rose to $2.5M, largely because of a $569K bad-debt write-off tied to a non-responsive UK customer. “As a precaution, we have decided to write off the receivable this quarter… and have filed a lawsuit,” Wieck explained, framing it as a necessary cleanup step. The write-off, combined with higher legal costs and Brazil investments, pushed the quarter to a net loss of ($0.03) per share, versus a $0.04 profit last year.

Despite the earnings dip, the outlook remains strong. KLNG highlighted five significant contract wins across subsea tiebacks, control equipment, flying leads, and cable management, driving its record-high backlog. Wieck noted that customer feedback from the U.S., Brazil, and Norway suggests subsea tieback activity “may become significantly higher than previously anticipated,” aligning with rising global demand. With this backlog base, he said the company now has the flexibility to “strategically test and optimize price points” to lift profitability going forward.

From a thesis perspective, nothing really changed for me this quarter. The market’s reaction feels similar to prior periods where investors overreact to a lumpy print and forget that no real business grows in a straight line. What I actually like here is how management handled the write-off — openly, immediately, and without burying it in adjusted metrics. To me, that’s not weakness; that’s clearing the weeds now so the path ahead is clean. And if they collect the money later, that becomes pure upside optionality.

More importantly, the bigger picture still looks healthy: record backlog, renewables momentum, expanding service demand, and early success in Brazil. I don’t see a business losing momentum — I see one preparing for operating leverage and margin recovery once the backlog converts. For context, I did trim about 30% of my position at the end of October because the allocation had gotten too large. But after this quarter, with the long-term setup intact, I’m seriously considering adding those shares back.

They Just announced another contract — a significant fabrication award tied to offshore/subsea work. Execution starts immediately at their Houston facility and runs through Q1 2026.

EVLV — Evolv Technologies

I like Evolv because security has become a real, unavoidable priority across public venues. Unfortunately, the world we live in today requires better screening solutions that don’t ruin the experience for people attending games, concerts, or theme parks. With massive global events like the World Cup coming this year, the need for fast, non-intrusive, and scalable security systems is only going to increase. Evolv sits right at the intersection of safety, technology, and throughput, which is why adoption keeps growing across stadiums, arenas, and entertainment venues.

From a technical standpoint, the stock also looks interesting here: moving averages are compressing and the price has been consolidating for a while, even as the underlying business continues to expand. For me, this is more of a trade at these levels, but one that has a real chance of turning into a long-term investment if execution continues and adoption keeps building. That expansion is showing up in real life — Evolv continues to stack high-quality wins in sports and entertainment, with recent deployments like Pechanga Arena San Diego, alongside well-known venues such as SoFi Stadium, Crypto.com Arena, the Hollywood Bowl, and Oracle Park. Management recently noted that Evolv now has nearly 100 sports and entertainment customers worldwide, reinforcing the idea that this is a solution gaining real traction at large, high-traffic venues.

REOP

ACFN — Acorn Energy

I re-entered the stock on December 19 around $5.15 and tweeted about it at the time. The entry made sense to me from a technical analysis standpoint, and shortly after, this PR dropped from Acorn Energy.

While the press release is fairly open-ended and doesn’t spell out anything concrete yet, I still see it as positive news. To me, it’s a signal that management is actively looking for ways to support and accelerate their ~20% growth target, particularly across infrastructure assets like cell towers, data centers, and utilities.

I also recently watched a presentation suggesting that an $80/share outcome by 2030 could be achievable using very conservative assumptions. Obviously, execution matters, but between the improving technical setup and management clearly pushing to expand the opportunity set, I think this is a name worth paying attention to again.

OPXS

FSI — Flexible Solutions

Flexible Solutions turned in a decent top-line this quarter: revenue was $10.56 million, up ~13% year-over-year ($9.31 million in Q3 2024). That growth came despite headwinds—tariffs, higher cost of goods, and startup costs tied to their new food-grade contract. CEO Dan O’Brien stated: “In Q4, substantial revenue from the food contract has been generated and Panama has finished improvements leaving only final equipment installation and testing prior to startup later this year.”

However, profits took a step back. The company recorded a net loss of $503,358, or ($0.04) per basic share, compared to net income of $611,858 ($0.05 per share) in Q3 2024. Management attributed much of the loss to the preparation costs for the new food-grade business (installation, training new shifts, etc.), and higher tariffs and raw material costs. These are one-time or transitional in nature, though they do weigh on near-term margins.

Strategically, the story remains interesting. FSI is moving into the food-grade manufacturing space (large contract announced, production ramping), expanding their Panama factory for tariff-avoided production, and maintaining their legacy biodegradable polymer business. As O’Brien said: “While it would have been wonderful to achieve all this without a net loss for the quarter, it was not possible.” The implication: they’re investing now, accepting short-term pain for longer-term optionality. If execution goes to plan, revenue and margin upside could follow.

PXHI — PhoneX Holdings

No recent news.

KTEL — KonaTel

KonaTel’s quarter was mixed on the surface — revenue of $2.17M is still down year over year — but the underlying business is finally cleaner, leaner, and more focused. The IM Telecom restructuring removed meaningful recurring costs, the company collected $850K of its $1M holdback, and management trimmed another $600K in annualized expenses. CPaaS is becoming the real engine here, with wireless POTS installations up 20% sequentially and long-term demand tied to the national copper-line shutdown. For the first time in a while, the core business and IM Telecom aren’t tripping over each other, and KTEL has multiple lanes (SMS, IoT, POTS replacement) showing early momentum.

But the real catalyst — the one that matters more than any quarterly metric — is the California healthcare partnership. As CEO Sean McEwen put it, the model is capital-light: “we bear no financial burden for sales, marketing, or equipment.” This channel began promoting Lifeline to Medicaid customers in October, and its scale potential dwarfs everything else in the business. If adoption accelerates the way management expects, the partnership could fundamentally reset KTEL’s revenue base without the drag of customer-acquisition cost. In short: the company itself looks structurally healthier, but the stock hinges almost entirely on how quickly — and how broadly — this healthcare-driven Lifeline channel ramps.

MOJO