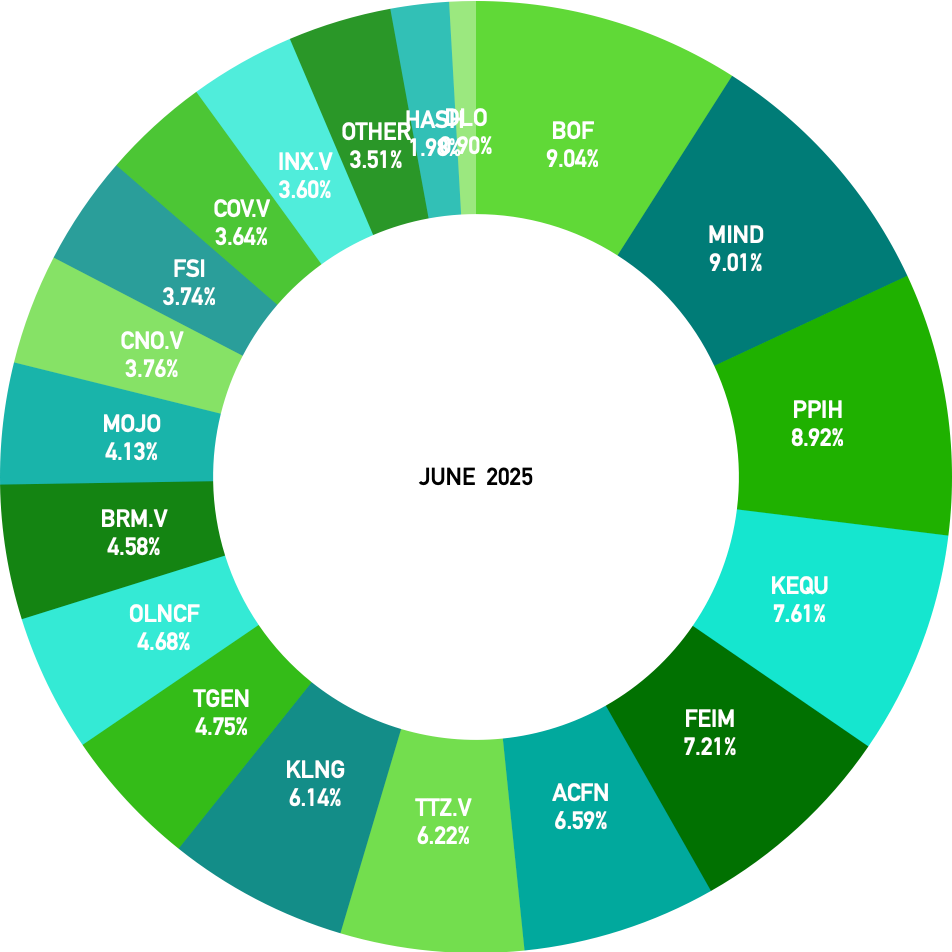

June Update

Disclaimer

This is my personal analysis, written to track companies I’m interested in, as of June 28, 2025. It is not financial advice, and I’m not recommending buying, selling, or holding any stock. I may or may not own shares, and readers should do their own research before investing.

BOF - BranchOut Food Inc.

MIND - MIND Technology, Inc.

PPIH - Perma-Pipe International Holdings, Inc.

KEQU - Kewaunee Scientific CP

FEIM - Frequency Electronics, Inc.

ACFN - Acorn Energy, Inc.

TTZ.V - Total Telcom Inc.

KLNG - Koil Energy Solutions

TGEN - Tecogen Inc.

OLNCF - Omni-Lite Industries

BRM.V - Biorem Inc.

MOJO - Equator Beverage

CNO.V - California Nanotechnologies

FSI - Flexible Solutions International, Inc.

COV.V - Covalon Technologies LTD

INX.V - Intouch Insight

OTHER

HASH - Simply Solventless Concentrates

DLO - DLocal

Hey everyone,

The portfolio rebalanced itself from where it was in May, with winners growing larger and losers shrinking, but June turned out to be a real eye-opener, particularly with $HASH, which I’ve been reflecting on after mentioning Ian Cassel’s article “No One to Blame” on X. I was pretty bummed since it took up a decent slice of my portfolio and hit me hard, and what’s sticking with me most is how I didn’t dig into my own research enough—I got too comfortable with the positive takes from people I follow, only to see even those sharp investors get tripped up too. I overlooked clear warning signs, like negative cash flow paired with positive net income—a red flag I now see, especially since Mathiew from Stocks and Stones had pointed it out many times, a lesson I’m determined to learn from. Meanwhile, the Middle East conflict this month drove home how crucial it is to back solid companies with healthy balance sheets and honest management—tough to find, but key for weathering unpredictable black swan events. Thankfully, it wrapped up by month’s end, though these surprises can boost some companies while dragging others down, and with a strong portfolio, it’s easier to hold steady.

Selling at a loss is tough for me, but after chatting with Gustavo @mexicaninvestor, he convinced me it’s worth it to reallocate what’s left into my top convictions. He shared how cutting losses quickly turned his performance around, so I took his advice and trimmed the underperforming “other” segment. I also sold $BIRIDF, even though I like their potential and had a solid profit—there are just too many other opportunities out there right now. On the flip side, I added more to $BOF, $FSI, $TTZ, $TGEN, $CNO.V and $MIND, and I started a position on $DLO, (introduced by Gustavo) the company serves as a vital toll bridge for global e-commerce in emerging markets, streamlining complex local payment systems and regulatory challenges through a single API integration. Operating in regions like Latin America and Africa, dLocal enables seamless transactions where payment methods are localized, regulations are dynamic, and financial infrastructure is limited. The company boasts a strong financial position, with $637 million in cash and equivalents, minimal debt, and consistent profitability in both net income and cash flow. Pedro Arnt, dLocal’s CEO and former CFO of Mercado Libre for 12 years, holds a 4.8% stake in the company’s Class B shares.

Big movers for the month:

POSITIVE

BOF 0.00%↑ +25%

FEIM 0.00%↑ +17%

FSI 0.00%↑ +15%

KEQU 0.00%↑ +57%

TGEN 0.00%↑ +44%

NEGATIVE

$HASH - 55%

BOF - BranchOut Food Inc.

Here is a great presentation from the company presented on the Micro Cap Club, if you are interested in the company this will be very helpful

https://microcapclub.com/branchout-food-bof-an-emerging-player-in-the-natural-foods-space/

MIND - MIND Technology, Inc.

PPIH - Perma-Pipe International Holdings, Inc.

KEQU - Kewaunee Scientific

In recent months, Kewaunee Scientific Corporation (KEQU) has faced significant headwinds, with its stock price dropping due to tariff uncertainties, DOGE-related funding cuts, and broader market concerns affecting research-focused companies. However, the Trump administration’s proposed cuts to NIH funding, which target “indirect costs” such as lab maintenance and utilities, are unlikely to directly impact KEQU. The company’s products, including laboratory furniture and equipment like fume hoods and workstations, are funded through direct project budgets, which remain largely unaffected. CEO Thomas D. Hull, III, emphasized the company’s resilience, stating, “Kewaunee again delivered another strong quarter, closing out fiscal year 2025 on a high note,” highlighting their ability to maintain momentum despite challenging conditions.

The market responded enthusiastically to KEQU’s Q4 2025 results, with the stock price soaring approximately 35% the following day. This surge reflects strong financial performance, with Q4 sales reaching $77.1 million (up from $56.7 million year-over-year) and full-year 2025 sales climbing to $240.5 million from $203.8 million. The company’s order backlog grew to $214.6 million, up from $155.6 million the previous year, signaling robust demand. KEQU’s acquisition of Nu Aire, a leader in laboratory equipment such as biosafety cabinets, further strengthens its position. Hull described the acquisition as uniting “two market leaders with complementary strengths,” expanding KEQU’s product portfolio and enhancing market resilience. With $17.2 million in cash, a debt-to-equity ratio of 0.99-to-1, and a strategy for both organic and inorganic growth, KEQU is well-equipped to navigate uncertainties and drive future growth.

TTZ.V - Total Telcom Inc.

Q3 2025 was a solid quarter. Sales climbed 48.8% to $660,955 from $444,063 in Q2, driven by race management fees (up $100,000 from last year, thanks to new All-In-One racing units) and growing Water-TraX hardware sales. Operating income swung to $106,114 from a $41,408 loss in Q2.. Net income doubled to $77,983 from $37,904, though a $24,181 loss from a weaker US dollar cut into Q2’s $65,220 currency gain. Gross margins stayed steady at 58.8% (vs. 58.4% in Q2), and expenses ticked up to $198,007 from $190,105, mainly for Water-TraX marketing.

operating cash flow fell to $414,637 for nine months from $637,902 last year. The Q3 report points to working capital: receivables rose to $290,139 from $236,235 as sales grew, meaning clients are paying slower. Meanwhile, payables dropped to $165,722 from $202,625, so they’re paying suppliers faster. I think this comes from their white-label model, where they partner with big clients like RV or industrial brands who take longer to pay, while suppliers want cash quickly. It’s a temporary cash flow squeeze, but their strong sales and profits keep me confident.

$3M in cash, only invested $83,416 in term deposits (vs. $1,359,065). In Q2, they warned US tariffs could hurt RV controller sales, which dropped to $153,000 in HY 2025 from $430,000 in 2024. Q3 shows a recovery—$271,000 for nine months—so tariffs haven’t hit hard yet, but they remain a risk for higher costs or lower demand. This cash reserve allows them to explore new markets and stay flexible. Plus, their April 2025 heater controller IP sale ($70,000 USD plus $25 per unit royalty) is a brilliant move, boosting recurring cash flow with minimal spending.

I estimate recurring revenue is about 30% of sales (~$477,000 of $1,588,774 for nine months), based on my earlier analysis. It has high margins (~80%), and hardware sales (~50% margins) cover $587,748 in expenses while driving growth. With a $5.02M market cap, $3M cash, and just $539,624 in liabilities, they’re trading at ~7x EV/EBIT

Tariffs, currency swings (37% of cash in USD), and reliance on third-party providers are risks, but their cash and lean setup give them room to maneuver.

CNO.V - California Nanotechnologies

In FY2025, Cal Nano demonstrated impressive growth, with full-year sales reaching $6.22 million, an 87% increase from $3.34 million in the prior year. Fourth-quarter sales also rose to $1.15 million from $0.98 million in Q4 2024. However, EPS remained flat at $0.00 for both Q4 and the full year, compared to $0.01 in the prior year, reflecting significant investments in infrastructure and operations. CEO Eric Eyerman highlighted the company’s focus on scaling manufacturing services and securing recurring commercial orders, which began in April 2025. These efforts aim to enhance predictability and diversify revenue streams, particularly through the new Santa Ana facility, positioning Cal Nano for sustainable long-term growth.

Despite a strong FY2025, Cal Nano faces challenges in Q1 FY2026 due to reduced activity from its green steel customer, which accounted for 63% of FY2025 revenue but has significantly declined following the completion of R&D targets. The company is actively addressing customer concentration risks by diversifying its client base, with early progress shown in Q1 FY2026. Cal Nano invested over $2 million in equipment in FY2025 and fully repaid its debt to Omni-Lite Industries, eliminating “going concern” status. Looking ahead, management anticipates reduced capital spending in FY2026, focusing on improving equipment utilization and contribution margins. While short-term volatility is expected as the company expands its customer base, Cal Nano’s strategic investments and diversification efforts signal a promising outlook for future growth.

The rapid pivot to diversify revenue is a critical and commendable step for Cal Nano, especially given the risks tied to its previous reliance on a single major customer. Building a diversified portfolio of new commercial clients will likely take time, as establishing stable, recurring contracts requires careful cultivation of relationships and consistent performance. I’m optimistic about the direction they’re heading as they work toward a more balanced and resilient revenue base.

INX.V - Intouch Insight

Intouch Insight Ltd. $INX.V / $INXSF announces acquisition of ClearPoint Solutions US, LLC assets for $250K USD, with potential profit-sharing over 4 years. Expected to close July 3, 2025. A strategic move to boost merchandising market presence

HASH - Simply Solventless Concentrates

The company presented its Q4 results on June 3, and they weren’t great—there’s a lot of info and analysis out there explaining what went wrong, so I won’t dwell on it. Then, on June 6, SCD released an interview with Paul Aundreola and Jeff, CEO of HASH, where he laid out what “really happened.” To me, those accounting issues should’ve been addressed way earlier, and the CEO not bringing it up feels off. Even if the numbers look better now, the excuse that “it’s always been done this way” doesn’t hold water for me. On June 20, they shared Q1 results, and while the market opened with a positive reaction but, it ended the day in the red. I’m still pretty new to investing and have already dealt with 70% drops, and in my short time, I’ve noticed it’s tough for a company to bounce back when it doesn’t respond well to what looks like good news in the short term. So, I’m thinking it might take a while for a recovery—if it happens at all. Still, I’m holding my shares—I’m already down big and not ready to panic sell. I’ll probably sit on them for a few quarters to see if things improve, then decide to sell, which I suspect a lot of others are thinking too.

On June 16, SSC announced a partnership with California-based Natura Life + Science to bring the popular Sluggers cannabis brand to Canada, launching premium pre-rolls like Bubble Bath and Fire OG in July. With exclusive distribution rights, SSC will use its subsidiary ANC Inc.’s manufacturing strength to tap into Sluggers’ U.S. success—top pre-roll sales in California and 600% vape growth—keeping 75% of net income from Canadian sales.

Occ (included in “Oters”)

Optical Cable Corporation (NASDAQ: OCC) reported Q2 2025 net sales of $17.5 million, an 8.9% increase from $16.1 million in Q2 2024, with the EPS loss narrowing to $(0.09) from $(0.21). Gross profit surged 32.1% to $5.3 million, lifting margins to 30.4% from 25.1%, fueled by improved manufacturing efficiencies and higher volumes. Backlog rose to $7.2 million from $6.6 million, reflecting robust demand, particularly in specialty markets like military, while enterprise markets held steady. However, rising SG&A expenses to $5.7 million and prior inconsistent execution suggest caution, though management’s optimism for the second half, as CEO Neil Wilkin stated, “We remain focused on disciplined execution and capitalizing on growth opportunities to drive shareholder value,” points to potential upside.

The conference call underscored OCC’s operational leverage and strategic focus, with Wilkin highlighting growth in Tier 2 and Tier 3 data centers, though hyperscale markets remain out of reach due to product differences. International demand and U.S.-based manufacturing offer advantages, with tariffs impacting OCC’s supply chain less than competitors. While seasonality typically drives stronger second-half sales, the company avoided specific guidance, noting product mix as a critical factor for future margins. Investors will look for sustained execution to confirm OCC’s ability to capitalize on data center opportunities and its diversified portfolio in a recovering industry.

Recommended articles/podcast

FEIM - Frequency Electronics, Inc.

Ive found this write up on FEIM if you are interested in the company, this deffinetly deserves a read. Personally ive done pretty nice in FEIM is my better perfromer in my portfolio, currently up around 130%. And even though its up pretty nice, im considering in increasing my position here.

DLO - DLocal

https://seekingalpha.com/article/4796545-dlocal-a-toll-bridge-in-payment-processing-for-emerging-markets

Interviews

Maj Souedian

Ian Cassel

Platforms every small- and micro-cap investor should use:

GeoInvesting / MS Microcaps LLC

MicroCap Club

CommonSenseInvesting